After three consecutive years of negative returns, Hong Kong’s property prices appear to be bottoming out, carrying wealth-effect implications for the local economy and across the Greater Bay Area (GBA). Despite representing just two percent of the overall land bank, Hong Kong’s commercial real estate (CRE) is worth between a third to one half of the GBA’s overall property market, based on analyst estimates, underscoring the city’s valuation delta and swing factor role in shaping regional dynamics.

Given limited inventory and greater appeal to international investors, Hong Kong’s CRE commands a pricing premium, notes Alan Tse, chief investment officer of Hong Kong-based AA Capital, speaking to The Bay. With the HKSAR accounting for a fifth of the GBA’s economy, Tse says any GBA property recovery requires an upbeat assessment of Hong Kong, where signs of an early CRE rebound are emerging in select pockets.

Population inflows supporting Hong Kong CRE

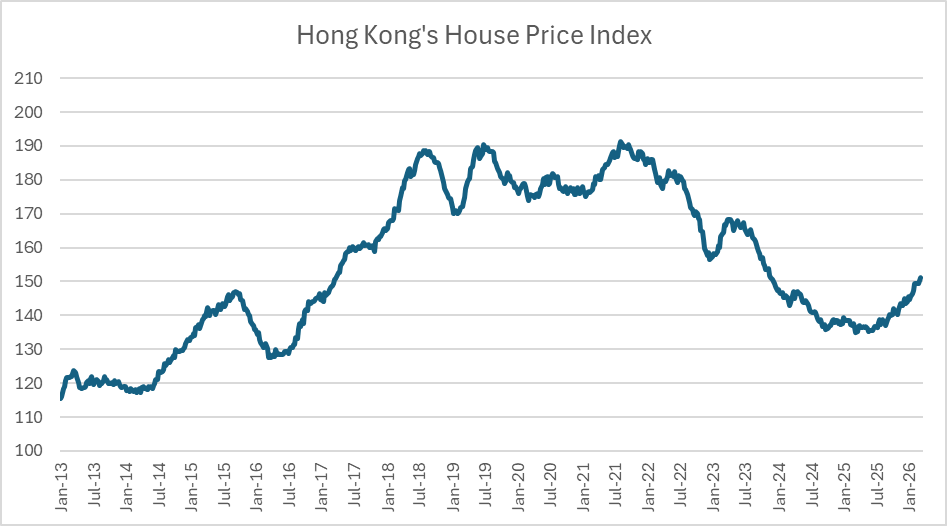

Home prices have begun trending higher over the past year. Though the city’s residential index remains a third below its 2019 levels, analysts are citing better affordability and favourable yield spreads which are encouraging renters to become buyers. With home prices having risen 4 percent year to date, Morgan Stanley expects the trend to continue, forecasting residential values to rise 10 percent and another 8 percent for 2027.

[See more: Hong Kong residential prices to rise 10 percent this year, says Morgan Stanley]

These changes are taking place as steady population inflows are generating new sources of demand. Improving academic standings at Hong Kong’s major universities have attracted a growing number of international students, with hotels and commercial buildings being refitted for student accommodations. Meanwhile various talent schemes have drawn nearly 180,000 people annually, mostly from mainland China, according to estimates by Jefferies.

As residential homes are being filled, so too are office spaces, particularly high-end workspaces adjacent to central business districts that have benefited from Hong Kong’s robust capital market activity. In 2025, the Asian financial hub topped league tables, raising $37.4 billion across 119 listings, marking the exchange’s strongest showing in five years and surpassing the combined volume of the prior three.

With the exchange announcing more than 400 companies waiting to go public, expectations for another record year are pulling investors into the office segment, according to CBRE’s 2026 Asia Pacific Investor Intentions Survey. Analysts have also cited the Middle East conflict as a secondary factor luring capital into the region, or at the very least, dissuading some funds from going abroad Tse says, reinforcing Hong Kong’s competitiveness for office spaces.

Rest of the GBA

But while momentum builds behind Hong Kong’s CRE recovery, headwinds remain across the GBA, mirroring a broader nationwide sluggishness in CRE demand. In the mainland GBA cities of Shenzhen and Guangzhou, rents continue to trend lower, however Shenzhen’s transaction volumes did rise last year while Guangzhou’s secondary market appears healthier than it was in 2020, according to a presentation by Kathy Lee, head of research and retail consultancy at Colliers, which was delivered at BritCham Macao’s property outlook last month.

[See more: Centaline Property expects 10 to 20 percent growth in Macao’s 2026 housing sales]

Lee meanwhile expects Macao’s property landscape to face steeper challenges, where record breaking tourism numbers and three consecutive years of positive gaming revenues have yet to impact other sectors of the economy. Retail sales have fallen for two straight years, while more than half a million square feet of office space are set to enter the market before the end of this decade. The new supply comes as office vacancies now stand at 20 percent and valuations have fallen more than 40 percent from their 2015 peak.

Industry harbingers

The Colliers presentation flags both weak demand and rising supply from neighbouring Hengqin as key challenges for Macao, raising questions whether comparable trends could emerge elsewhere, including Hong Kong. Retail units outside major tourist spots on Hong Kong island and the Kowloon peninsula continue to grapple with local market conditions, including a three-year high unemployment rate of 3.8 percent while warehouse rates are expected to decline this year by 8 percent.

However, AA Capital’s Tse says such concerns are misplaced for now, noting that any price correction seen is not market failure but rather a deliberate structural adjustment aligned within Beijing’s policy intent.

[See more: Greater Bay Area emerging as Asia-Pacific’s next nexus of growth, says top economist]

“The government has long viewed the GBA, including Hong Kong and Macao, as the pioneer for this economic rebalancing, where the supply expansions in areas like Hengqin serve as a mechanism to enforce the shift and pivot wealth creation away from property speculation and towards innovation, advanced manufacturing, and cross‑border financial integration,” he adds.

These developments are unfolding as both SARs are strengthening their economic capabilities, with Hong Kong reinforcing its role as a “global superconnector” for the Asian region, while Macao advances its 1+4 diversification initiative to broaden its tourism offering.